Black Book Market Update

Wholesale Prices, Week Ending May 8th

This past week marked fifteen consecutive weeks with the overall market increasing. Of those fifteen consecutive weeks, nine had increases of at least 1%. With the global microchip shortage and other supply chain disruptors forcing OEMs to alter their new car production, it is expected that this elevated market will continue throughout the summer. Remarketers are raising floors and holding firm with this knowledge that the supply is tight and will remain that way.

Car Segments

- Car segment gains ticked up slightly this past week (+1.25%) compared to the week prior (+1.17%).

- Five of the nine car segments had gains exceeding +1.00%.

- For many weeks, the Sub-Compact (+1.15%) and Compact Car (+1.56%) segments have been seeing the largest increases, but this past week, the largest gainer was the Mid-Size Car segment (+1.62%).

- The Luxury segments gains have slowed but are still large compared to normal seasonal patterns. Typically, these segments would be declining this time of year and rarely see increases, even during the spring market.

- Sporty Cars continue to see large week-over-week gains with an increase of +1.19% last week.

Truck Segments

- Truck segment gains increased this past week (+0.98) compared to the previous week (+0.89%).

- All thirteen truck segments reported gains last week, with five exceeding +1.00%.

- Sub-Compact Crossovers (+1.56%) and Minivans (+1.46%) had the largest Truck segment gains.

- Small Pickups resumed greater than 1% weekly increases (+1.31%) after slowing down to 0.94% two weeks ago. Full-Size Trucks (+1.22%) have averaged a weekly increase of +1.39% over the last nine weeks.

- The Luxury crossover/SUV segments have slowed the rate of gains, but for comparison, in 2019 these segments were declining.

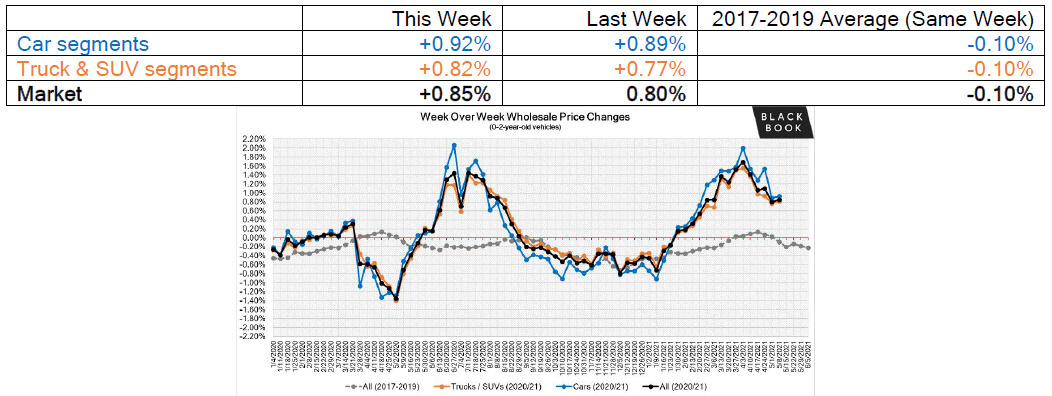

Newer Used Vehicles (0-2-year-old)

Driven by an extreme shortage of rental returns and limited inventory of new vehicles, the price trends of newer used vehicles have been experiencing larger weekly gains compared to the older units. Within the last three weeks, newer used units reached levels that, in some cases, exceed new car pricing while the rate of growth has slowed for older units. For example, in addition to F150 Raptor, 2020-21 Chevrolet Corvette, and 2021 Jeep Gladiator and Wrangler, dealers are paying above MSRP for 2021 Kia Telluride and Hyundai Palisade, as well as other mainstream models.

The table below shows the average weekly price changes for 0-2-year-old vehicles.

Weekly Wholesale Index

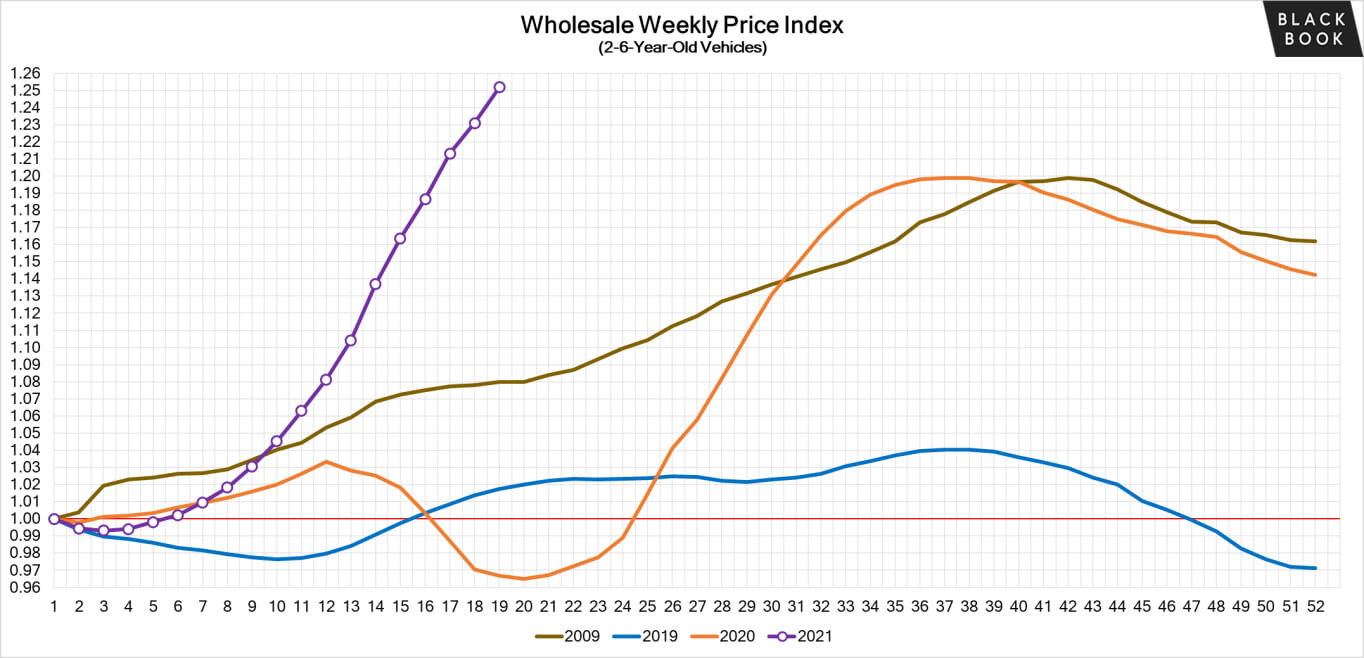

2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g. 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. It is now clear that 2021 will also not have typical seasonality patterns as the market is going through a rapid increase in wholesale values. The spring market arrived about 7 weeks earlier and with much stronger price increases compared to a typical pre-COVID year. The graph below looks at trends in wholesale prices of 2-6-year old vehicles, indexed to the first week of the year. Currently, wholesale prices are more than 25% higher compared to the beginning of the year (adjusted for the mix).

Black Book Monthly Retention Index

The Black Book used vehicle Retention Index shows another increase in March, continuing the trend of the last 4 months. The April Retention Index broke yet another record, reaching 152.4 points.

Retail (Used and New) Insights

- April new car sales were up compared to last year, but this is no surprise as this time last year is when the auto industry was hardest hit as a result of the COVID-19 induced stay-at-home orders. The SAAR for April hit 18.5 million. (1.66 million for Canada)

- As North American buyers have transitioned to SUV and crossover loving buyers, automakers have been forced to adjust their product offerings. The latest to announce changes to their line-up is Rolls-Royce with the discontinuation of the Dawn convertible and Wraith coupe after the completion of the 2021 model year. However, they do have plans for a release of an all-electric model in the future.

- The disruptions to the supply chain are getting costly for the manufacturers. Ford is estimating the microchip shortage is going to cost them $2.5 billion. Volkswagen revised their yearly earnings forecast after a strong Q1, but also cautioned on the negative impact that the reduced output, as a result of the shortage, will have on their second quarter profits.

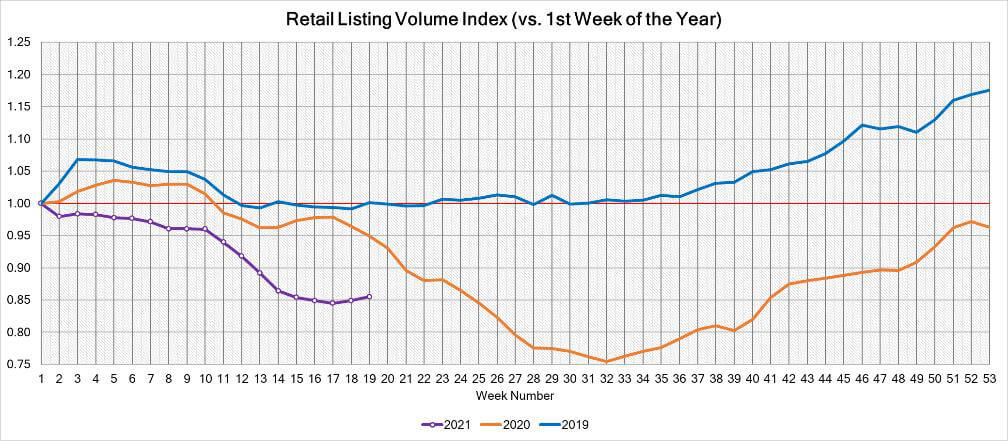

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices over the last several weeks of 2020. As demand rebounded in January, retail prices seemed to lag wholesale prices – retail asking prices continued to decline throughout January and remained stable in February. March had an accelerated growth in retail prices, but the rate of growth is still lower compared to the increases of wholesale prices. In April, retail prices picked up speed as demand accelerated, fueled by stimulus payments, tax season, and shortages of new inventory. Currently, the prices are more than 13% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles (similar to our wholesale price index).

Volume

Used Retail

Current used retail listing volume is about 15% below the start of the year, but the inventory levels stabilized in the last 4 weeks.

Days-to-turn have been decreasing since the middle of March, as retail demand picked up across the country due to tax returns and the additional round of $1,400 stimulus checks deposited into consumers’ bank accounts.

Wholesale

- Conversion rates have been declining over the last few weeks as the quality of inventory being offered for sale continues to decline. It is getting harder for buyers to find average or better condition grade vehicles.

- Condition of units has been the hot topic with buyers in recent weeks, as there are fewer average to clean units available. When buyers do find one, they are having to pay top dollar to secure it. For everything else, their reconditioning costs are increasing to ensure they get the units retail ready.

- With the ongoing new inventory shortage, the availability of used units is expected to remain tight throughout the summer, especially with rental and fleet companies holding their units in service longer until replacements are available. New inventory levels are not anticipated to recover until 2022 due to the ongoing supply chain issues.

Originally posted on F&I and Showroom