Weekly Market Update Report

Wholesale Prices, Week Ending May 1st

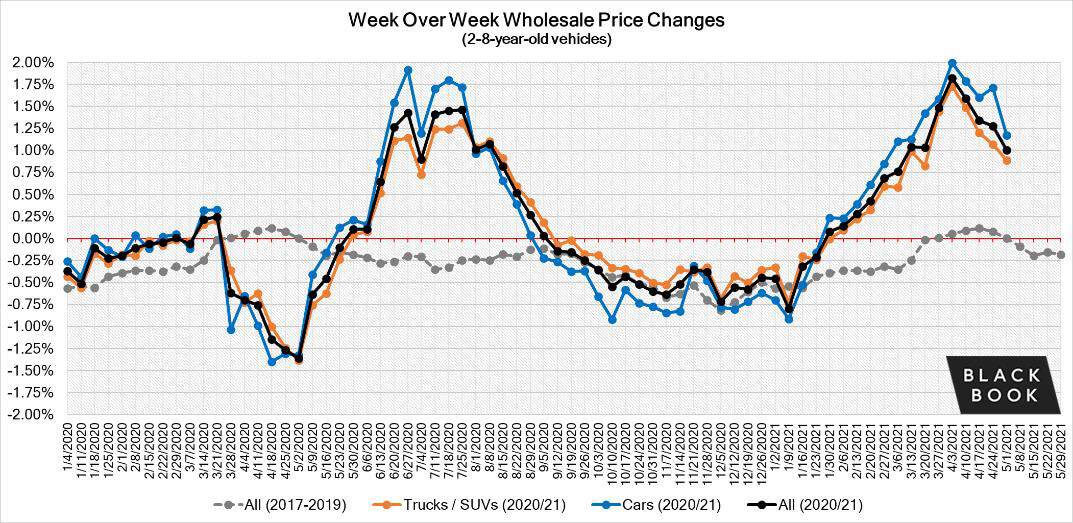

Wholesale values continue to rise, but the rate of increase is shrinking each week. However, the value increases are still considered extremely large for single week gains compared to a “normal” market. Retail inventory levels, new and used, continue to be a challenge and the limited availability of quality vehicles in the wholesale market is also proving to be a challenge for buyers.

This Week Last Week 2017-2019 Average(Same Week)

Car segments +1.17% +1.71% -0.05%

Truck & SUV segments +0.89% +1.07% +0.04%

Market +1.00% +1.28% +0.00%

Car Segments

- Car segment gains slowed this past week (+1.17%) compared to the week prior (+1.71%).

- For the first time since mid-March, all nine Car segments did not have gains exceeding 1% and none broke the 2% mark.

- Despite Compact Cars (+1.74%) having a lower week of increases last week, the average weekly increase for the past seven weeks is a staggering +2.17%.

- Full-Size Car (+0.99%), Luxury Car (+0.83%), and Prestige Luxury Car (+0.62%) were the only three Car segments to not increase more than 1%, but these are still well above normal seasonal changes. During this same week in 2019, Prestige Luxury (-0.48%) and Luxury (-0.32%) segments both declined.

Truck Segments

- Truck segment gains continued this past week (+0.89%), but it was at a lower level compared to the previous week (+1.07%).

- All thirteen truck segments reported gains last week, with four exceeding 1%, compared to nine segments increasing more than 1% the week prior.

- Sub-Compact Crossovers had five consecutive weeks of increases exceeding 2%, but this past week the rate of gains slowed to +1.62%.

- Small Pickups broke their streak of eight continuous weeks of increases exceeding 1% with this past weeks’ gains slowing to +0.94%. However, Full-Size Truck increases (+1.11%) are still exceeding 1%.

Newer Used Vehicles (0-2-year-old)

Driven by an extreme shortage of rental returns and limited inventory of new vehicles, the price trends of newer used vehicles were experiencing larger weekly gains compared to the older units. Within the last three weeks, newer used units reached levels that, in some cases, exceed new car pricing while the rate of growth has slowed for older units. For example, in addition to F150 Raptor, 2020-21 Chevrolet Corvette, and 2021 Jeep Gladiator and Wrangler, dealers are paying above MSRP for 2021 Kia Telluride and Hyundai Palisade, as well as other mainstream models.

The table below shows the average weekly price changes for 0-2-year-old vehicles.

This Week Last Week 2017-2019 Average (Same Week)

Car segments +0.89% +1.54% -0.05%

Truck & SUV segments +0.77% +0.93% +0.07%

Market +0.80% +1.09% +0.02%

Weekly Wholesale Index

2020 ended with used wholesale prices at elevated levels. With economic patterns (including the automotive market) driven by the pandemic, normal seasonal patterns (e.g. 2019 calendar year) in the wholesale market were not observed for most of the year. We saw a similar picture in 2009, at the end of the Great Recession. 2021 will not have typical seasonality patterns as the market is going through a rapid increase in wholesale values. The spring market arrived about 7 weeks earlier and with much stronger price increases compared to a typical pre-COVID year. The graph below looks at trends in wholesale prices of 2-6-year old vehicles, indexed to the first week of the year. Currently, wholesale prices are more than 23% higher compared to the beginning of the year (adjusted for the mix).

Retail (Used and New) Insights

- The global microchip shortage has now idled Ford plants in Mexico, one of which produces the newly released Bronco Sport compact crossover. This closure is just one that is plaguing the manufacturer with the overall shortage threatening to potentially force Ford to cancel half of their Q2 production plans. General Motors is also being forced to idle production of one of their top-selling models, the Equinox, at its manufacturing facility in Ontario for two months.

- Up until now, BMW has remained safe from the microchip shortage, but they’ve now announced their first plant closure in England that is responsible for the X1 and X2.

- Carvana is continuing to grow with this past week’s announcement of their expansion into seven new markets, including cities in Utah and Alabama.

- The chip shortage isn’t the only ongoing threat to production. Toyota had to halt Rav4 and Lexus RX production at their facility in Ontario due to a COVID-19 outbreak at a supplier’s plant.

Used Retail Prices

With the proliferation of ‘no-haggle pricing’ for used-vehicle retailing, asking prices accurately measure trends in the retail space. Retail demand slowed down at the end of last year, and thus resulted in declining retail asking prices over the last several weeks of 2020. As demand rebounded in January, retail prices seemed to lag wholesale prices – retail asking prices continued to decline throughout January and remained stable in February. March had an accelerated growth in retail prices, but the rate of growth is still lower compared to the increases of wholesale prices. In April, retail prices picked up speed as demand accelerated fueled by stimulus payments, tax season, and shortages of new inventory. Currently, the prices are more than 10% above where we started the year.

This analysis is based on approximately two million vehicles listed for sale on US dealer lots. The graph below looks at 2-6-year-old vehicles (similar to our wholesale price index).

Volume

Used Retail

Current used retail listing volume is about 15% below the start of the year, but the inventory levels stabilized in the last 4 weeks.

Days-to-turn have been decreasing since the middle of March, as retail demand picked up across the country due to tax returns and the additional round of $1,400 stimulus checks deposited into consumers’ bank accounts.

Wholesale

- Conversion rates remain strong, but the poor condition of many of the available vehicles at auction currently is a deterrent for buyers and has resulted in a small decline in sales percentages on some lanes with these lower quality units in recent weeks.

- Available inventory on dealer lanes has improved in recent weeks, as more dealers are taking their trade-ins to auction to take advantage of the strong wholesale demand. Despite the low inventory on the lots, the margins that can be made at their local auction is too good to pass up.

- With the ongoing new inventory shortage, the availability of used units is expected to remain tight throughout the summer, especially with rental and fleet companies holding their units in service longer until replacements are available. New inventory levels are not anticipated to recover until 2022 due to the ongoing supply chain issues.

Originally posted on F&I and Showroom