Joe Raedle/Getty Images News

The following segment was excerpted from this fund letter.

Carvana (NYSE:CVNA)

The Portfolio first bought Carvana in Q3’19. I wrote about the Carvana investment thesis last quarter so I will try to keep my comments brief, although it has been the largest stock price decline and biggest impact on our results year-to-date so it deserves some further discussion.

Looking out into the future it seems inevitable that more used cars will be bought and sold online. If we break down the ~40 million used cars that are sold each year, it seems probable that ~5-10 million of that total will be bought/sold online. In fact, one could argue a higher share given how much better the entire customer value proposition is in terms of selection, lower online retail cost structure at scale, and overall buying/selling convenience and experience. However, that would require addressing older and higher mileage cars and more off-lease vehicles.

E-commerce and much of the internet-related services have a winner-take-most type dynamic. Having the greatest selection and infrastructure provides a better customer value proposition, which drives more demand, enabling greater selection and infrastructure investment. There is typically little room for a number two player within the same vertical offering a similar service, especially if the leader has a strong head start.

In the used car market, selection is not the only major problem to be solved for customers. If it were, CarGurus (CARG) would take the cake. Buying and selling used cars is full of customer pain points. Solving them takes the ability to seamlessly integrate a wide selection of vehicles that customers can trust are the actual quality that they expected at purchase, convenient and consistent delivery, streamlining financing of a high-priced item, all in a self-service intuitive consumer interface.

Carvana is building what is truly an impressive and difficult-to-provide integrated customer value proposition. However, this means little if Carvana is not able to reach scale because of the massive capital requirements needed to build this infrastructure as well as endure operating losses until reaching scale.

Its service requires building inspection & reconditioning centers (IRCs), inventory levels, its transportation network, technology in car buying/pricing, the user interface, and advertising which all require a ton of upfront capital. The difficulty with a company like Carvana is that it essentially needs to be a nationwide business from day one. To be successful, its service needs to be available everywhere and therefore has to scale fast.

In the last letter, I discussed how retailing has evolved over time into ever higher operating leverage business model which requires greater initial capital investment. At scale it can provide greater inventory turns at lower gross profit margins therefore attractive returns on invested capital. Walmart (WMT) required more upfront capital than a mom & pop store but was still able to realize attractive store economics relatively quickly. Amazon required much greater upfront investment to provide its service across the country.

Even CarMax (KMX), which is widely considered to have attractive economics for its industry, had a somewhat disruptive and more capital-intensive model compared to traditional used car dealers. When it was trying to scale its service and systems in the 1990’s, it incurred seven years of initial losses before reaching profitability, financed by its parent company Circuit City.

Up through 2021, Carvana was blitzscaling as it grew unit volumes and the needed infrastructure as fast as possible. Customer demand for Carvana’s service was not the issue, it was having enough supply to be able to serve growing demand. Management prepared and hired for anticipated demand about six months in advance which worked well until Q1’22 when industry-wide used car volumes began to decline.

When combined with winter storms, a resurge of COVID leading to high workforce call-off rates, and a rising rate environment squeezing the spread on their financing gross margins, Carvana experienced unexpected losses.

On top of the Q1’22 losses Carvana acquired ADESA in May, further leveraging its balance sheet by raising $3.3 billion of debt. The acquisition price appears high if compared to the $100 million it brings in expected EBITDA. However, the cost savings to Carvana by having the ADESA locations, particularly throughout the West Coast and Midwest, is material. For example, California currently makes up around 10% of the used car sales within Carvana’s existing markets but the closest inspection and recondition center (IRC) is in Phoenix.

The closest IRC to Washington or Oregon is Salt Lake City. Delivering a car from Phoenix to a market in California could be up to a 1,500-mile round trip depending on the market. Delivery costs and transport times can be substantial. IRCs that are within 200 miles of customers save ~$750 per unit vs. the average transaction.

For markets like California or Washington where customers can be much further from an IRC, savings are even greater. ADESA provides numerous locations throughout the western U.S. that provide Carvana the network density to immediately simplify last-mile delivery and eventually fill out its IRC network much faster than previously possible.

If there truly is a winner take most dynamic to online used car retail and this is a very large market to address, then acquiring ADESA’s attractively located properties today makes a lot of strategic sense for long-term success. Carvana’s total operating losses do not provide a clear picture of the growing value of the company and its true earnings power. What is far more insightful are the unit economics and whether there is a strong customer value proposition with earlier cohorts providing early indications of reaching positive EBITDA margins.

Of course, Carvana must get to scale to succeed and therefore requires capital to bridge the time until cash flow from operations is more than sufficient to support the company. After raising $3.3 billion in debt and $1.25 billion in equity in Q2’22, Carvana has $1 billion in cash and $4.7 billion in liquidity. Even during a prolonged macro weakness in used car sales, Carvana faces little solvency risk with enough liquidity to maintain operations for at least 2-3 years without needing to raise further capital.

We are not investing in Carvana today and expecting it to pay us dividends within the next year. We are investing in Carvana today because we want to own a piece of a company that is highly likely to be the dominant online used car retailer far into the future. If that scenario unfolds over the next decade or two, the dividends that Carvana will be able to pay out to shareholders will be multiples of its current market cap.

{kind=link}

|

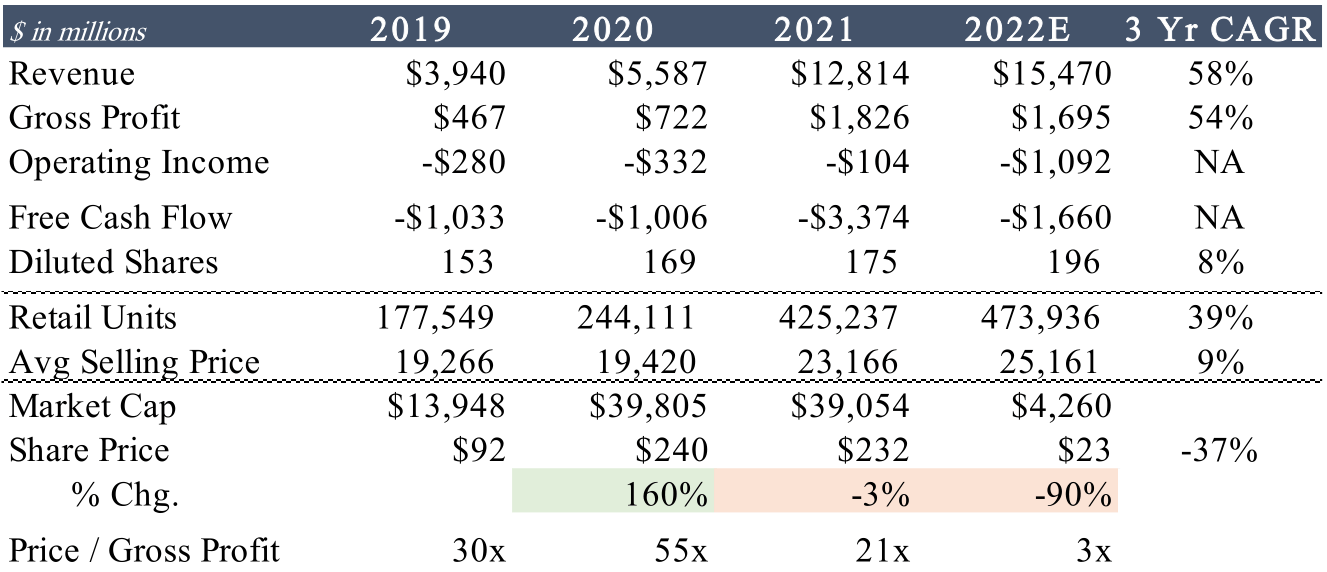

Source: Company filings, Factset, Saga Partners Note: 2022E values are Factset consensus expectations, market cap and share price are as of 6/30/22. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.